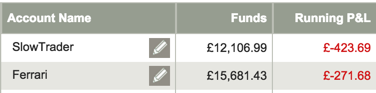

For simplification, I’ve combined Slow Trader and Ferrari into one fund which we will refer to as Slow Trader Fund.

Our strategy in Slow Trader is to short term trade (using, primarily, daily close bars rather than intra day bars) shares in the FTSE 350, stocks in the S&P 500 and major foreign exchange (FX) currency pairings.

Arm Holdings. We came out at a little over break even. I moved our stop as I was not happy with the possible trend change of this share price. The share price did move below our buy point but has subsequently moved up again. We are out for the time being.

Halliburton Co. We set this share stop also to a little over break even. This took us out without lose and the share price has continued to drop. A good move on our part.

BT Group. Moving the stop too early is usually not a good thing. I feel that the stop should only be moved if something happens to make you change your mind about the share or the share price has climbed sufficiently to put you into a different price bracket. I got this wrong with BT. I moved the stop and got stopped out for £17 profit but the share turned and continued up!

Ashtead Group. – £311 lose. On reflection, not a good share to take. A ranging share price, rather than my strategy of taking trending prices, this share dropped well below my entry price – but has subsequently turned up again.

CLS Holdings. – £325 lose. I made fundamental mistakes with this one. Incorrect retracement level without price action. If I had waited (patience is the virtue of a good trader) and measured the retrace correctly this could have been a winner.

I bought at the red arrow, the green arrow was of course the correct buy point.

I bought at the red arrow, the green arrow was of course the correct buy point.

Card Factory. – £311 lose. This is a relatively new share. Only 5 years of fundamental information, I prefer 10 years.

We were in credit – having bought at the lower green arrow – but a sharp drop took us out. You will notice that I sell a share for a lose (or more accurately, I’m stopped out if a share price drops below what I think is acceptable).

FX AUD/USD. + £394. This is the first time you have been introduced to FX. This is on an intra day 4-hour chart so you can see the move.

We bought at the red arrow, we sold at the green arrow and we bought again (and we are still in) at the blue arrow. Easy! Okay, sometimes it goes ideally like this.

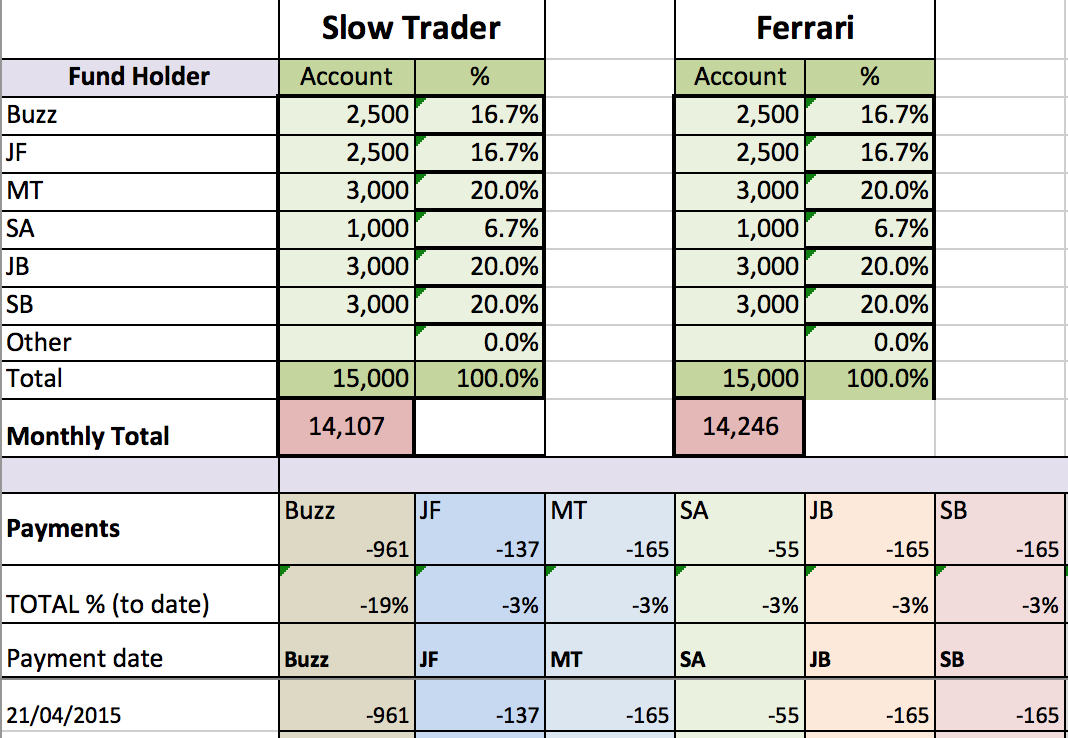

We also had interest charges (mostly for carrying shares over the weekend) of – £32.

We are currently in:

CLS Holdings. We bought again at the green arrow on the CLS chart above. Although the price has moved up we are still -3.7 points as this is the spread. The spread is how the broker (in our case IG) make their money. It is the same as when you go on holiday and change your sterling for euros, you have a buy and a sell rate.

ITV PLC. + 2.6 points.

Money supermarket. + 12.1 points.

Monster Beverage. + 568 points.

Underarmour. + 464 points.

WPP PLC. – 9 points.

FX AUS/USD. – 20.9 points.

Finally, anyone wishing to short term trade for themselves I am trialling a notification system to help you. You will get my information direct to your smart phone so you will need an account that you can action through your phone. More later.

B