Those of us that want to technically trade the financial markets for a living, or simply make a profit doing so, have undoubtedly invested a lot of time, money and emotional effort into the process.

There are, however, certain aspects that, no matter what our chosen trading method, seem to be hurdles for us all.

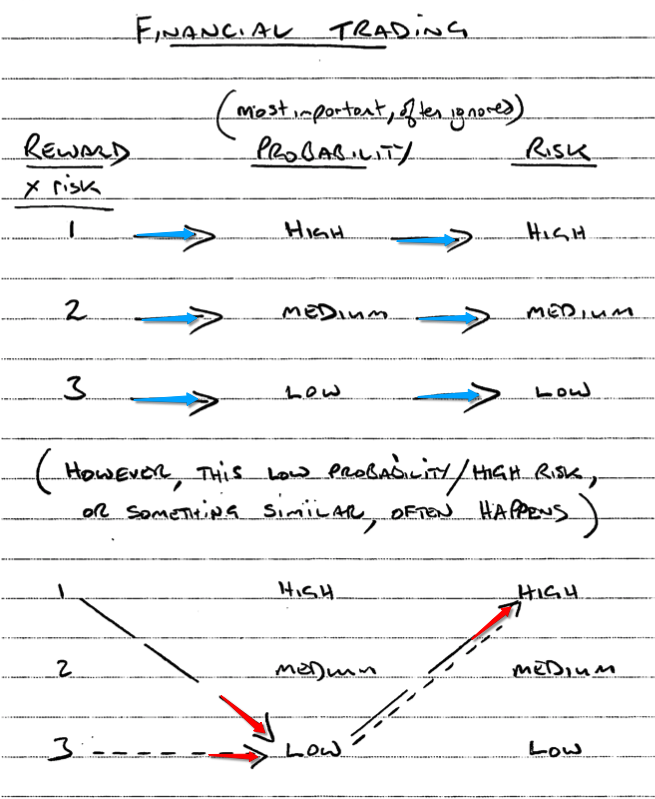

Trading, for example, is full of contradictions: we need to hold our winning trades, but we need to know when to take profits; we need to make a traders equation, but we need wide stops; and we need to wait for a clear signal, but the so-called clear signals often don’t work.

A few trading conditions that I struggled with, and still do from time to time, include: not holding the trade all the way to target; entering on a whim of a signal, or worse no signal at all; and, my unfortunate favourite, trying to reverse a trade too early.

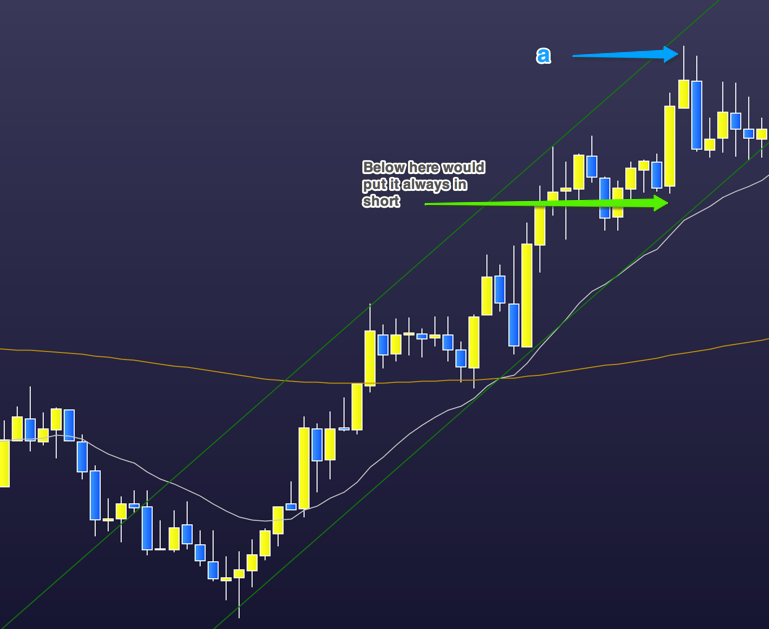

The latter is probably the single reason most traders struggle. I have an example trade from yesterday where (this time) I correctly held the trade from the currency pairing USD/JPY.

Firstly, I have to say that context is a big part of my trading strategy. When I show these snips we are not showing the overall context. That is: what price was doing leading up to the few bars we show on the chart. Five minute bars in this case. In this instance over the last two days the market had been in a steep descent, or bear trend.

We can see that the market turned bullish and went long in what seems to be three pushes (marked on the chart). After three pushes the market often reverses. For me the market was always in long after the 1st push and I looked for opportunities to get long.

At this point a novice trader, influenced by the prior two-day bear market, and not trading in the moment, would be entering short at the top of both push 1 and 2 hoping for a resumption of the bear.

I exited my long at the blue arrow marked ‘a’. Choosing the exact exit from my long position was, of course, fortuitous. I thought, correctly this time, that price may reverse early and before price could hit the green channel line which I’ve drawn.

However, price did not pull back as expected and at the yellow circle, which I’ve marked on the chart, I re-entered long. I exited that long, at a measured distance of the previous leg, for a reasonable additional profit. This turned out to be a ‘final flag’ long.

Reading the chart correctly, with the whole chart available, always seems obvious. However, reading bar by bar in a live trade is another thing altogether.

We are wary about entering long because of the steep bear trend on the higher time frame chart; and, to continue long when the bars are in the top right hand corner of our screen, provides its own psychological block.

To trade, as in this example, is often counter intuitive. Whether we use price action, indicators or a combination of both we can only make a profit if we trade by (expert) rules and not by emotion and intuition.