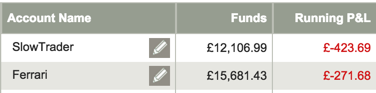

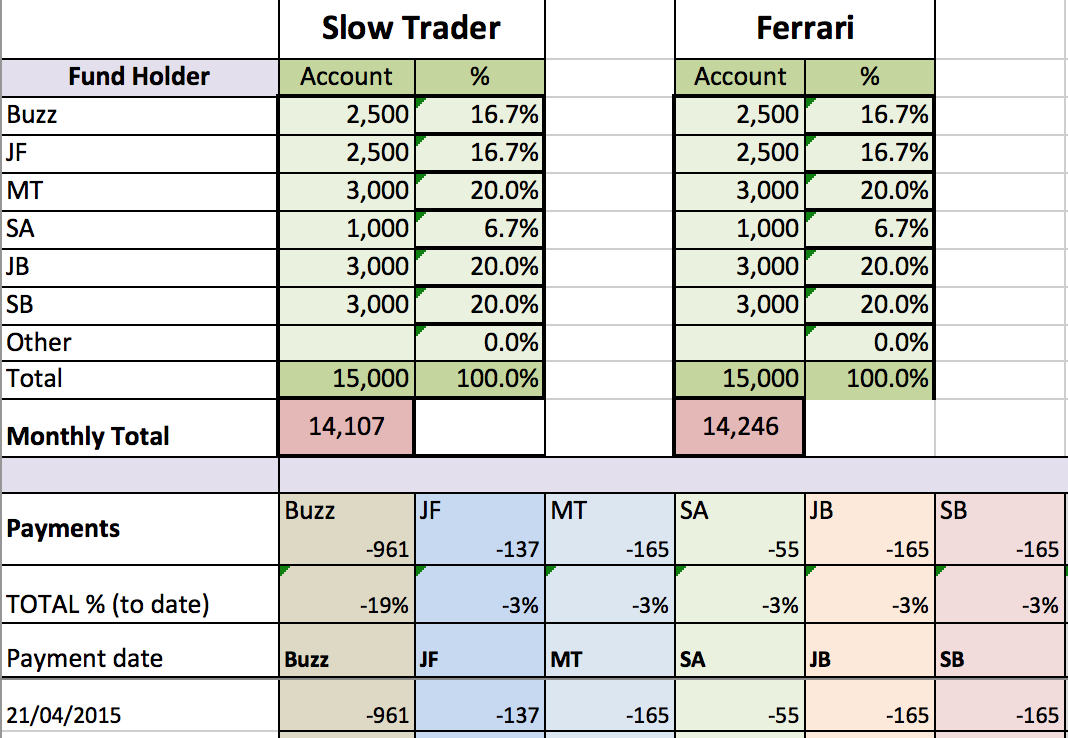

First of all, because of the holidays, the next fund report (Slow Trader and Ferrari Funds) will be about 23rd January 2015. With Slow Trader, we took a hit in the last report and we had 2 or 3 trades that were still to come off. These took us a good 10% lower than my last report. However, on the plus side we currently have several trades that are running and these are in profit. Let us see.

I’ve made simple but significant changes to our trading technique. In terms of timeline, I’ve come out more – now taking a broader view. To that end we will use the ‘futures style’ purchasing rather than the relatively expensive Daily Fund Bet. This will help to reduce our fund operational costs.

I’ve back tested weeks worth of trades to find the best timelines for our indicators. There is never a sure bet, if it were that easy…

However, I am confident that we have something that suits the current market. These things need regular review as what worked a while back might not necessarily work as well today.

I’ve titled this article – how to get the most from my retirement pot – because that is what I’ve been looking at recently. Primarily to find the best pension scheme for my small company and employees. The one I have chosen is http://bandce.co.uk/ the peoples pension.

Other than it being internet based, so no middle man, the pension is clear and easy to use and provides some great funds to choose from. More importantly, it only charges 0.5% with no other costs. The low charge over a 20 years or more is significant.

One of the problems with mutual or managed funds (including banks) is the high management cost of their funds. This is a secret the big funds have kept for decades. For every percentage charged in management you can deduct at least 20% from your final lump sum. If you’re keeping a fund for 40 plus years the percentage is higher than this. Therefore, a managed fund that is costing you say 2.5% will reduce your final award by some 50%. If your fund was due to pay out £100,000 then you would only get £50,000 – maybe as little as £35,000. You’re giving the fund managers potentially £65,000 – and for what!

How is this possible? Its all to do with that magical reason: compound interest. Probably the most powerful tool you can financially teach your kids, grand kids etc. If you want more proof of this read Tony Robbins recent book Money: Master the Game. Its a mammoth read but well worth it. Obviously the book uses American terminology, but the UK is similar with different names.

If not managed or mutual funds then how do I invest my money? Simple, self-managed index or tracker funds. This is something that will track a bunch of companies – say the FTSE 100 or S&P 500 – and will cost you very little to do so. In compound terms you keep that £65,000 rather than, as in the example above, give it to a bank or fund manager. Also, don’t let your broker suggest that a managed fund will get you more return over time for your money – your broker is not your friend. Over the last 20 years the stock or share market has gone up almost 10%. The average for managed funds has been about 2.5%. What a difference. Indeed, some 98% of managed funds do not beat the market – or, in other words, do not beat your self-invested index or tracker fund.

Diversification in funds is important. In our hedge funds, for example, I look carefully at sectors in turn. Careful not to overload in any one sector. An index fund, by its nature, invests through all sectors. How you distribute your money is individual depending on age, retirement goals, health. However, with 15 years to go before retirement be very cautious of being overly exposed to the share market. The reason is that, historically, the share market has taken belly churning drops twice in any 12 year period. The suggestion, therefore, of 15 years gives you a buffer. If you cashed in your fund in late 2008 you would have got nearly 50% less than a few months prior. Not good.

They don’t get a great press, but fixed annuities are a great way to go. Do not, however, go with the first suggestion from your pension fund if they provide an annuity. Shop around and get the lowest cost. Is a low cost annuity safe? After 2008 throughout the USA hundreds of banks went bust but not one insurance company (an annuity provider) went under.

I would split my retirement money as:

- Annuity

- Go-get-em or growth fund

- Fun fund

I would consider 60% of my funds with an annuity. Again, depending on personal funds and circumstance. That is your safe fund. Your income to live on and hopefully help pay the bills. Most of the remainder I would put in a growth fund or a ‘go-get-em’ fund. But of this I would put as much as 50% in gilts or bonds (with a mix of treasury and corporate and the bigger mix being long-term gilts or treasury bonds). Of the remainder of the go-get-em amount, I would put 30% in a cheap to run tracker or index fund: of the small remainder I would split between commodities and gold. My final, now small, chunk of my overall amount would be my fun fund. You might consider the hedge you have with me as your fun fund. The beauty of a hedge is that this fund loves it if the market goes up or down. Both are good. What it does not like is a flat market.

There you go, I hope that has generated some thought.

I recommend this 30 minute animation ‘How the Economic Machine Works’ – well worth 30 minutes of anyones time. http://www.economicprinciples.org/

Also, if you need to check out your state pension statement go to https://www.gov.uk/state-pension-statement

Have a wonderful Christmas and see you back here in the New Year.

B