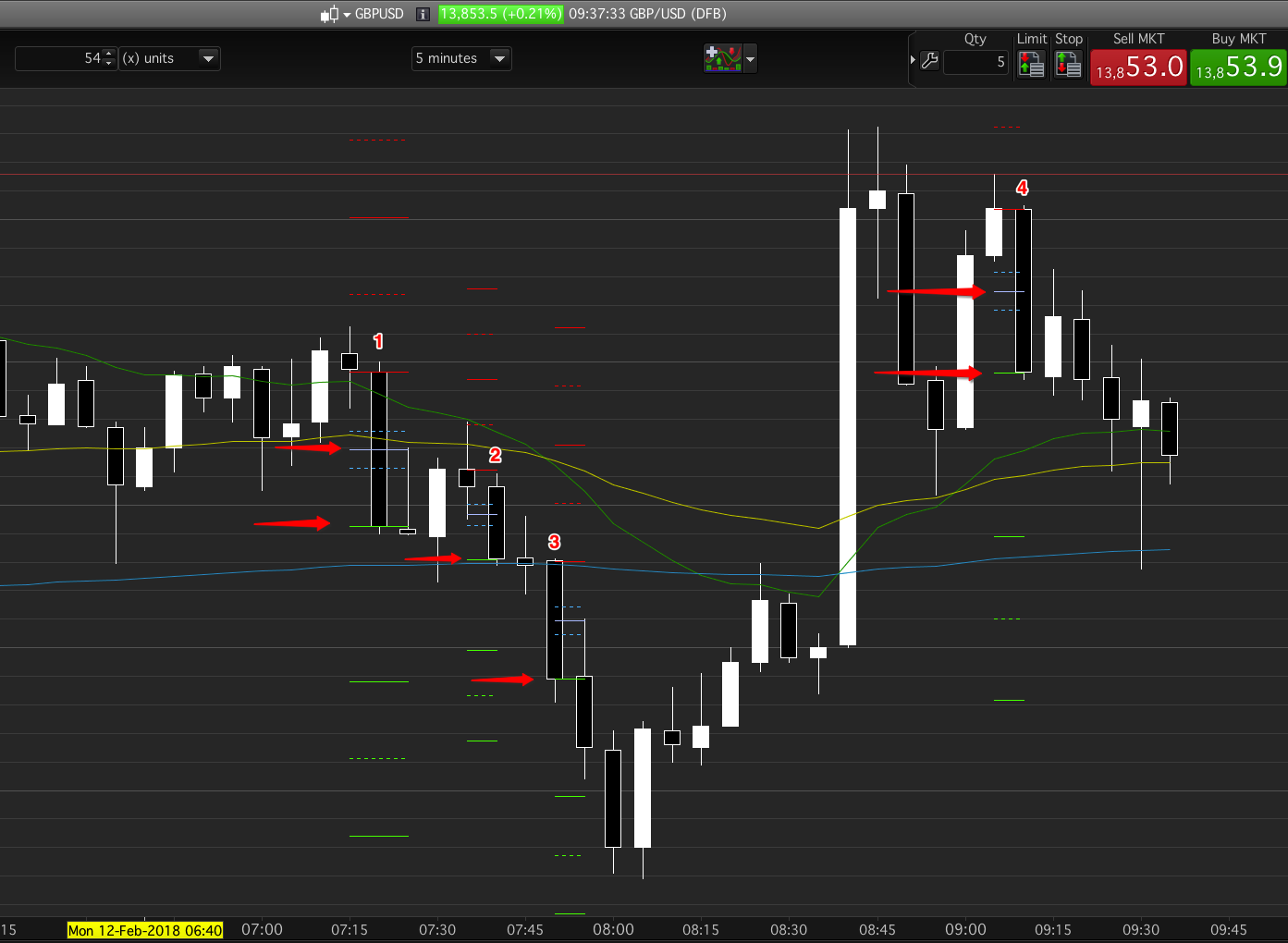

First trades of the day can often test our resolve. Bar 1 below was our early trade this morning (12th February 2018). The London market is starting, and this can introduce volatility. Moreover, we don’t feel settled into the chart, we have a possible wedge that could take the price long and as the day has no news to mention we could be in for a trading range day.

We place our limit order short at the close of bar 1 and at the midpoint of the same bar. The next bar, a pin bar down but not a new low, is not the follow through we were looking for. We exit on-market for a break even. Bar 2 and bar 3, on the other hand, provide confirmation of reasonable probability of at least a scalp short so we take our limit order shorts at the close of each; the midpoint pull-back limit entries were not activated.

Our initial trade (from bar 1) if we’d held it would have provided 27 pips of profit. Bars 2 and 3 entries combined provided 17 pips of profit.

Some traders would have taken the first bull bar long after bar 3, however changing trade direction that quickly is difficult. Bar 4 was our next opportunity. By now we were in the groove and entered at the close of bar 4 and at its midpoint. The subsequent scalp provided over 28 pips of profit.

Short entries were taken at each of the red arrows.