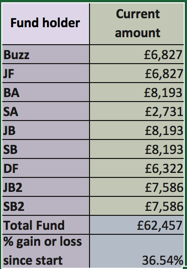

Our Slow Trader fund has sat on the fence for a few months waiting for me. Not being a boom and bust trader, I have traded small whilst developing our ‘probability trading’ technique.

A level of profitability through consistency has to be achieved before increasing trade size. The technique provides that, now it is up to me.

It may seem a bit odd that I’ve moved away from trading a market, US stocks, that has increased this year as an index 20 percent or so. UK shares not so much at 6 or 8 percent as an index.

To day-trade profitably I need to give it (day trading) all my attention. Having trades open in other areas and time frames were definitely a distraction for me.

Why have I chosen day trading despite the many stories that tell us not to trade this way? Bizarrely, it is control. As a ‘probability’ trader, we accept that we are trading a market that is random. In other words, we accept that anything can happen.

If we except that anything can happen, then we accept the risk. We accept that the market is only about a price that can go either up or down. In ‘probability trading’ we also accept that certain effects happen when lots of traders trade. Things happen that can give an observant trader an edge.

Despite the simplicity described, it has taken me a couple of years to combine price action trading and money management, specific entry and exit techniques, and group it all together, test it exhaustively and call it probability trading.

Fund contributors that think the share market, and particularly the US stock market, are to continue climbing throughout 2018 ought to withdraw their funds from Slow Trader and head that way.

After all, that is the market, with you, that Slow Trader originally entered.

If you stay in the Slow Trader fund, and to do so you don’t need to do anything else, you become part of a probability day-trader fund. Our advantage: we are not concerned about a good or a bad year for stocks and shares; we trade a currency pairing in the short-term, with an edge; with (to quote Mark Douglas) rigid rules and flexible expectations.

We have developed a day trading strategy that allows us to take money consistently – day in, day out. We scale-up though when we’re ready.