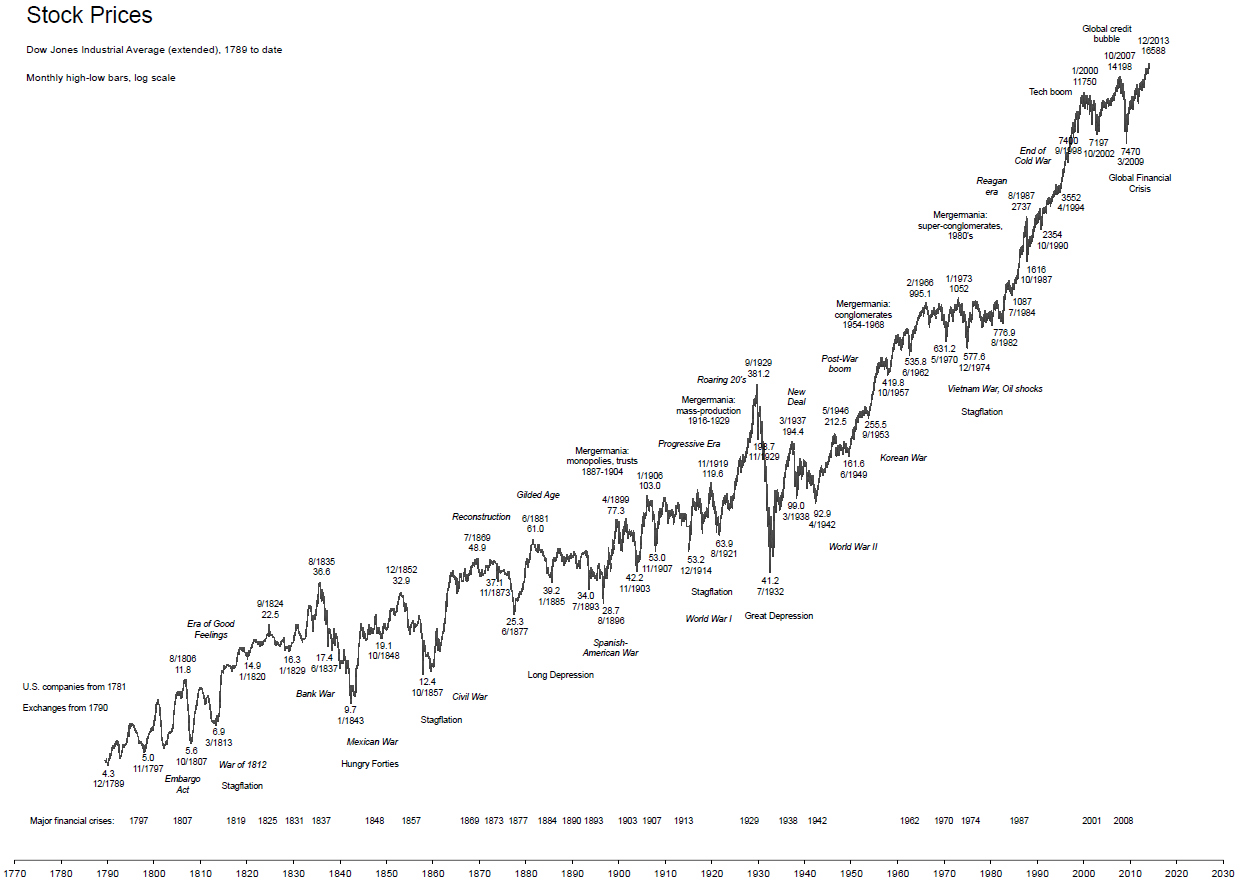

Here’s a long term historical chart. I love to look at this stuff. If someone bought at the top of the Great Depression in 1929 it would have taken until my birthday in 1956 to break even!

Here’s a long term historical chart. I love to look at this stuff. If someone bought at the top of the Great Depression in 1929 it would have taken until my birthday in 1956 to break even!

Blog

-

Long Term Historical Chart

-

Aveva Group PLC (UK AVV)

Aveva share price continues down and, therefore, did not take my last buy request at just above £21. As the price has now moved below its previous low on 18th December, I have cancelled this buy. I will watch from the sidelines for the time being on AVV.

Aveva share price continues down and, therefore, did not take my last buy request at just above £21. As the price has now moved below its previous low on 18th December, I have cancelled this buy. I will watch from the sidelines for the time being on AVV. -

Hargreaves Lansdown PLC (UK HL.)

Hargreaves Lansdown PLC are a provider of investment products to private investors in the United Kingdom.

Hargreaves Lansdown PLC are a provider of investment products to private investors in the United Kingdom.Recently voted Britain’s Most Admired Company within the specialty finance category.

Half-year results are very good. Record sales – but profit margin down slightly.

Active client numbers were boosted by Royal Mail shareholders who invested in the postal service through the group’s services.

Interim dividend has climbed, now 7p per share.

You might want to take advantage of the recent dip in HL. share price.

-

Aveva Group PLC (AVV)

We are approaching a good longer-term investors buy signal for Aveva, a computer software company for engineering solutions. I have set my buy today at £21.23. Remember that I will adjust this buy price if the share continues down. Note that the share is also trending down in the medium term, so those trading rather than investing may want to wait. -

2014

Whatever your style of investing or trading you would like to choose companies that are great and have a habit of growing.

Whatever your style of investing or trading you would like to choose companies that are great and have a habit of growing.We look for such companies. They are hard to find. Over the last few years many companies have grown rather well. Some of these companies have probably grown where they didn’t justify to do so. We like to put our money behind companies that are 10-years old or more with wonderful growth and at a big price discount.

We do not try to second guess the world economy. Because this is difficult to do. However, it is also hard to ignore Harry S Dent and Larry Williams, both of which I have followed for some 15 years. Dent looks at demographics and debt and Williams looks at indicators. Both are saying similar things for 2014.

I like it to taking a convoy of cars from Ambleside, in the Lake District, over Wrynose and Hard Knot pass. The cars represent companies. In 2009 you left Ambleside and went up Wrynose. On the way some cars had clutch issues and some had brake problems!

Many continued up. The sharp twists and turns of the road represented the share chart. It was exciting at times, but always up. For many of us we reached the top of Wrynoss, in late 2013. Lovely. To get out of the wind, in January 2014, we went over the top and stopped for a cup of tea. That is where we are now.

Williams, says we will walk back up to the top to take in the views. Both Dent and Williams say that at some point we will run back down to the cars and complete the journey down the other side. A few may have brake problems!

You are not the driver but a passenger. You feel committed but you can get out – sometimes easier said than done when you are already coming down the other side. Particularly if you’re blindfolded and unsure of the road ahead!

I’m not a financial advisor, nor do I want to be – see disclaimer. When I post a company that is when I look to buy or sell. I usually place a buy ahead of the share price so if the share continues up it will catch my buy, hopefully close to what I wanted. If the share goes down or flattens then my buy won’t be taken. I then rethink and probably reset my buy position. So, when I post a buy or sell on the blog it is not the complete picture, it is more involved than that. But as an investor the difference is usually minor.

I will soon be introducing US shares to the blog. This gives us more scope to find great companies and, of course, some US shares are household names in the UK.

I hope my 2014 analogy helps.

-

Domino’s Pizza UK & IRL PLC (DOM)

Could be a good time to take another “slice” of DOM. As we know the share has taken a fall over the last few months, not helped by the announcement of a change of Chief Financial and then Chief Executive Officer. However, the share price has risen nicely since then and now, after taking a small dip (possibly profit taking), the share price seems on the way up again. Not all my indicators point at a buy so I would only take a small bite at this stage.

Could be a good time to take another “slice” of DOM. As we know the share has taken a fall over the last few months, not helped by the announcement of a change of Chief Financial and then Chief Executive Officer. However, the share price has risen nicely since then and now, after taking a small dip (possibly profit taking), the share price seems on the way up again. Not all my indicators point at a buy so I would only take a small bite at this stage. -

Globo PLC (GBO)

Last week, Globo’s full-year trading update said they had achieved a strong financial performance for 2013, ahead of market expectations.

Last week, Globo’s full-year trading update said they had achieved a strong financial performance for 2013, ahead of market expectations.The telecom software products and services says revenues were up significantly boosted by growing sales of its GO!Enterprise development platform.

Globo said that it had seen continued demand for its consumer and enterprise products, buoyed by the growth of the bring-your-own-device trend in businesses.

The company said it is focused on expanding in Western Europe and the US via organic growth and acquisitions. Globo will make investment in sales and marketing to grow its customer base, and said it will focus on direct sales to end users towards the end of 2014.

Globo said that its current year trading had begun strongly, and expressed confidence that it will see another year of growth and market penetration as the bring-your-own-device trend continues.

The share has not moved much from my last post, 6th November 2013. If you missed that buy then this could be a good time.

-

Immundiagnostic Systems Holdings PLC (IDH)

We have a buy signal on IDH. One aspect of our buy signal is saying caution, however, worth taking some more of this share.

We have a buy signal on IDH. One aspect of our buy signal is saying caution, however, worth taking some more of this share.IDH have announced that they can enter the US market with their Direct Renin assay.

This is used to find the amount of active renin present in the blood. Results of the test are used to assist clinicians in the investigation of hypertension related disorders such as primary aldosteronism and renovascular hypertension. This is a fast and reliable alternative to existing manual methods, and a necessity when screening in extended hypertensive populations.

Hypertension is the third leading cause of death after malnutrition and diseases related to smoking. One in every three American adults have high blood pressure.

IDS first launched the automated Direct Renin immunoassay in Europe in June 2012.

-

Rightmove PLC (RMV)

This could be a good opportunity to top up with RMV shares. Buy back of own shares for RMV is in full swing over the next couple of months. 2013 was a good year for house price increases, particularly in London. However, January 2014 has seen a pause. RMV has excellent value potential in its share price and a recent dip might provide a buy opportunity. As yet, it is a little early on our indicators but a move back up could happen quickly. Be ready.

This could be a good opportunity to top up with RMV shares. Buy back of own shares for RMV is in full swing over the next couple of months. 2013 was a good year for house price increases, particularly in London. However, January 2014 has seen a pause. RMV has excellent value potential in its share price and a recent dip might provide a buy opportunity. As yet, it is a little early on our indicators but a move back up could happen quickly. Be ready. -

Advanced Medical Solutions Group PLC (AMS)

A good time to buy some more of AMS – At about £1.10. A medical technology company, selling advanced wound care products. They are debt free as of the end of 2013. Founding chairman of 16 years retired a few days ago. His replacement, Peter Allen (57), is external to AMS but experienced as a value creator within the health care industry. The global wound care market is worth $15 billion. The majority of sales by AMS come from their own brands. 450 employees. Products are manufactured from two sites in the UK, one in the Netherlands, two in Germany and one in Czech Republic. A growing company with excellent value left in their share price.

A good time to buy some more of AMS – At about £1.10. A medical technology company, selling advanced wound care products. They are debt free as of the end of 2013. Founding chairman of 16 years retired a few days ago. His replacement, Peter Allen (57), is external to AMS but experienced as a value creator within the health care industry. The global wound care market is worth $15 billion. The majority of sales by AMS come from their own brands. 450 employees. Products are manufactured from two sites in the UK, one in the Netherlands, two in Germany and one in Czech Republic. A growing company with excellent value left in their share price. -

Fisher (James) & Sons PLC (FSJ)

We have sold FSJ. Based on last years figures, share price is nearly at value.

-

How have we done?

Here is a list of our shares posted to-date with percentage increase/decrease in price over the last 3-months:

DOM 09 December 2013 18% RMV 05 December 2013 17% IDH 28 November 2013 12% PTEC 27 Novembere 2013 9% CRW 22 November 2013 24% AVV 18 November 2013 0% GBO 06 November 2013 0% TRCS 02 November 2013 16% DOM 25 October 2013 -5% AGK 25 October 2013 12% AMS 09 October 2013 26% TRCS 09 October 2013 8% AGK 09 October 2013 15% HL. 09 October 2013 49% FSJ 09 October 2013 20% AVERAGE 15% -

Naibu Global International Company PLC (NBU)

Naibu shows a buy indication at 77 pence.

Naibu shows a buy indication at 77 pence.

A Chinese manufacturer and supplier of branded sportswear, Naibu have traded on the London Stock Exchange for six years. They employ some 2,300. A growing company that allows you to invest in China but also, indirectly, in Chinese currency. The strength of Chinese Yuan to Pounds Stirling has contributed to Naibu’s decrease in share price over recent years. However, Pounds Stirling could be stabalising or even strengthening against the Yuan. This, in itself, could positively affect Naibu’s share price.

Naibu have 3,144 stores throughout central and western areas of China. By 2015 a new factory is planned to provide 12 additional productive lines and help Naibu expand into even more cities and provinces. They have achieved growing annual sales of about £100 million. More than half of sales are sports shoes, the remainder is clothing and a tiny amount is accessories.

They pay regular dividends. Naibu are openly seeking cooperation with international business partners. However, they had no major investments, acquisitions or disposals last year. Of possible note, the founding chairman recently sacked his CFO and appointed his sister in place.

They have no debt, and all other figures seem very good.

However, invest lightly. -

Domino’s Pizza UK & IRL PLC (DOM)

Domino’s Pizza Group (DOM) took a drop on Friday with the announcement that the Chief Executive Officer (CEO) would be leaving the company in April next year. (He was offered a bigger job in a non competitive area to Domino’s). Successor not yet announced. This was on top of the announcement last month of a change in Chief Financial Officer.

Domino’s Pizza Group (DOM) took a drop on Friday with the announcement that the Chief Executive Officer (CEO) would be leaving the company in April next year. (He was offered a bigger job in a non competitive area to Domino’s). Successor not yet announced. This was on top of the announcement last month of a change in Chief Financial Officer.Founded in 1960, Domino’s first UK store opened in Luton in 1985. A global, primarily franchised, system Domino’s has a single focus – The home delivery pizza.

There are now 750 stores in UK, 48 stores in Republic of Ireland, 25 stores in Germany and 10 stores in Switzerland.

More than half of sales are from online. And nearly half of these sales are from mobile devices. 50 new stores planned for the UK of which 23 are now open. In marketing, Domino’s recently partnered with the X Factor App.

Domino’s half year report had sales increasing nicely. They are expected to meet, or possibly exceed, Market expectations with their end-of-year report.

As you know, I have been a fan of this share for a couple of years. This dip could be a buy opportunity. Whether you are trading or investing you might like to wait until the share price shows a turn back up. A turn could be on the announcement of the new CEO and if he/she brings the right stuff!

Domino’s Pizza UK & IRL PLC