Whatever your style of investing or trading you would like to choose companies that are great and have a habit of growing.

Whatever your style of investing or trading you would like to choose companies that are great and have a habit of growing.

We look for such companies. They are hard to find. Over the last few years many companies have grown rather well. Some of these companies have probably grown where they didn’t justify to do so. We like to put our money behind companies that are 10-years old or more with wonderful growth and at a big price discount.

We do not try to second guess the world economy. Because this is difficult to do. However, it is also hard to ignore Harry S Dent and Larry Williams, both of which I have followed for some 15 years. Dent looks at demographics and debt and Williams looks at indicators. Both are saying similar things for 2014.

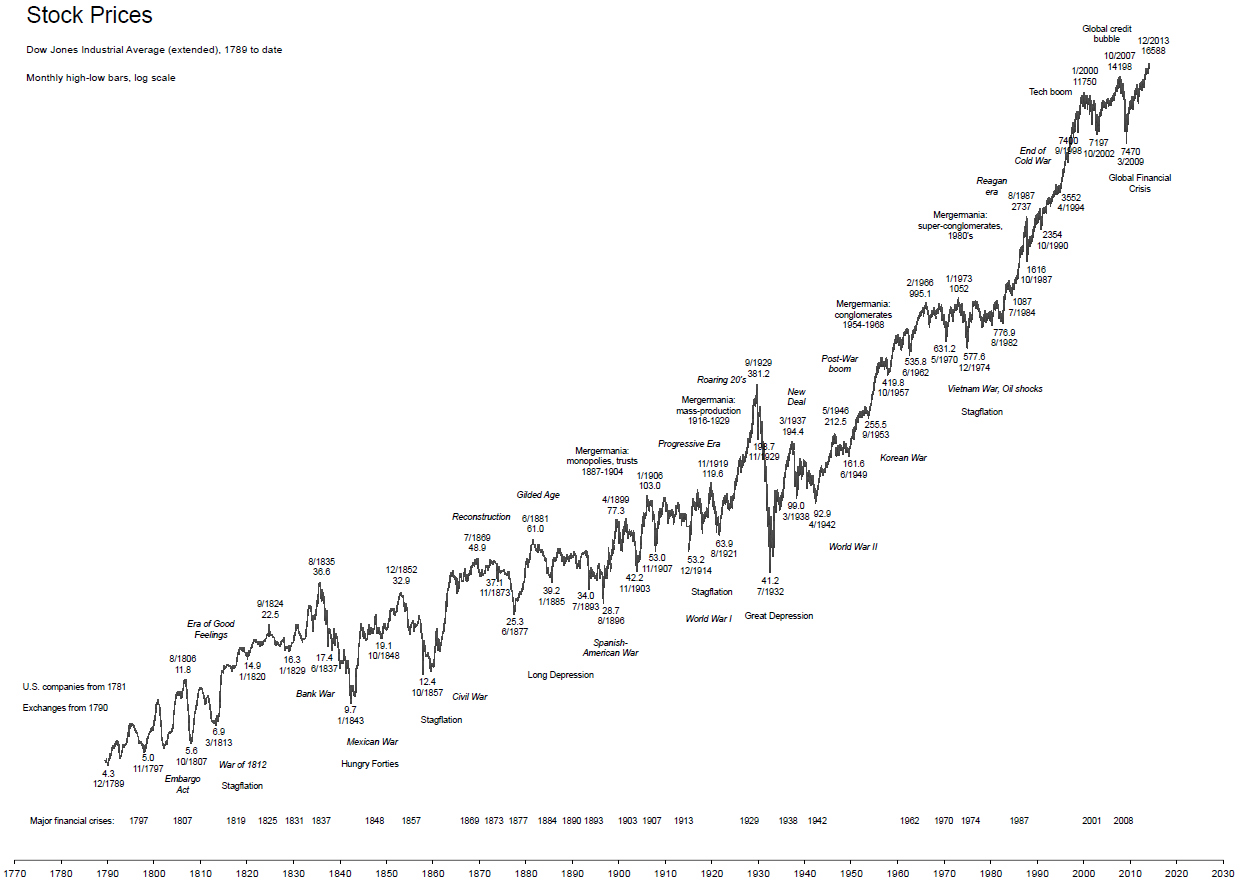

I like it to taking a convoy of cars from Ambleside, in the Lake District, over Wrynose and Hard Knot pass. The cars represent companies. In 2009 you left Ambleside and went up Wrynose. On the way some cars had clutch issues and some had brake problems!

Many continued up. The sharp twists and turns of the road represented the share chart. It was exciting at times, but always up. For many of us we reached the top of Wrynoss, in late 2013. Lovely. To get out of the wind, in January 2014, we went over the top and stopped for a cup of tea. That is where we are now.

Williams, says we will walk back up to the top to take in the views. Both Dent and Williams say that at some point we will run back down to the cars and complete the journey down the other side. A few may have brake problems!

You are not the driver but a passenger. You feel committed but you can get out – sometimes easier said than done when you are already coming down the other side. Particularly if you’re blindfolded and unsure of the road ahead!

I’m not a financial advisor, nor do I want to be – see disclaimer. When I post a company that is when I look to buy or sell. I usually place a buy ahead of the share price so if the share continues up it will catch my buy, hopefully close to what I wanted. If the share goes down or flattens then my buy won’t be taken. I then rethink and probably reset my buy position. So, when I post a buy or sell on the blog it is not the complete picture, it is more involved than that. But as an investor the difference is usually minor.

I will soon be introducing US shares to the blog. This gives us more scope to find great companies and, of course, some US shares are household names in the UK.

I hope my 2014 analogy helps.

As you know, IDH have been a past favourite of slowtrader. Nothing exciting to report on the company or its product: they sell immunoassay kits – many home pregnancy tests are immunoassays.

As you know, IDH have been a past favourite of slowtrader. Nothing exciting to report on the company or its product: they sell immunoassay kits – many home pregnancy tests are immunoassays.