I appreciate that we don’t have much time to read a blog, often on a mobile device and while we’re busy concentrating on something else. Meanings are easily misinterpreted. Moreover, true longer term ‘value’ investing is not a popular investment method. We want gratification earlier.

Someone close to me this weekend considered me wrong with the longer term investing methodology, suggesting that: (1) the market has changed and a five years investment model is long enough, (2) Buffett is an investing dinosaur and (3) proceeded to tell me why Blackberry really failed.

My initial explanation (blog) must have been poor, so I hope I can provide more clarification.

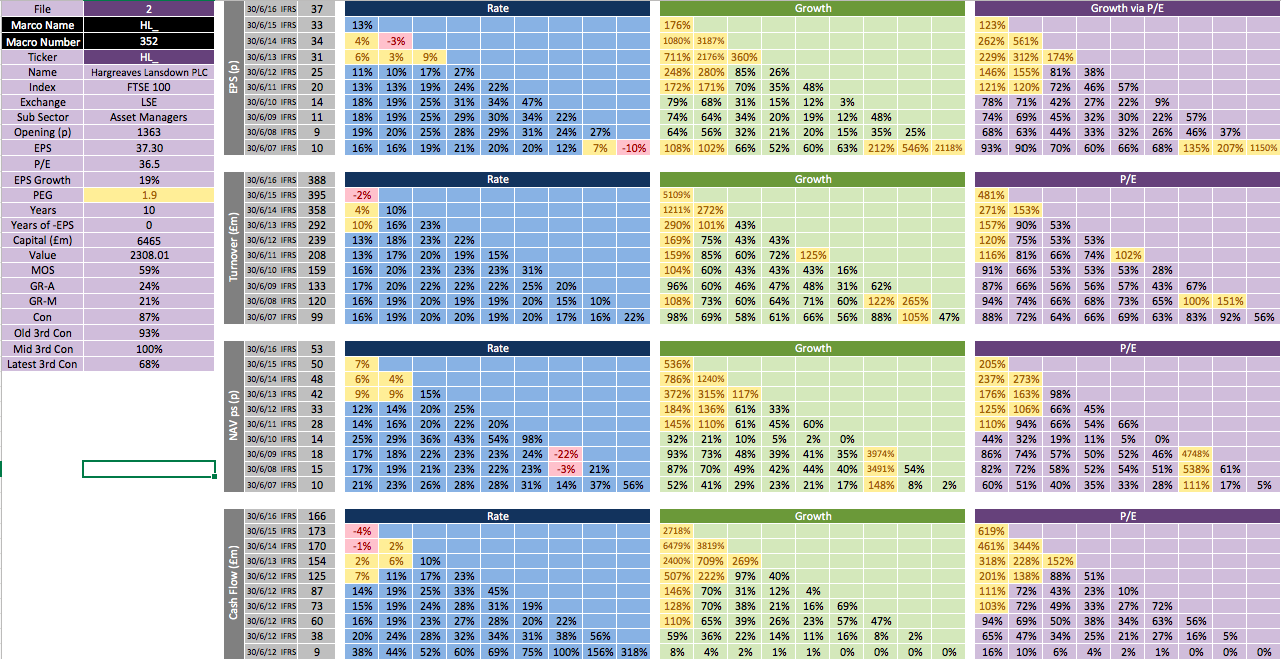

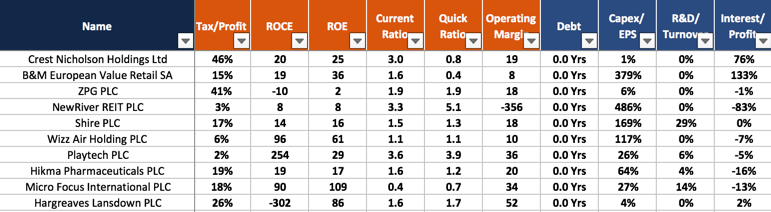

The numbers that we provided to back up the top ten shares can be confusing. We are looking for companies that ideally have ten years of reports showing no debt, a great consistency in growth and are available at the bargain price of fifty pence on the pound.

The latter refers to the margin of safety (MOS) that Graham coined. That is the same as being able to go to a BMW garage and purchase a £40,000 car for £20,000. A good deal. That is what the MOS is telling us. What it is not telling us is how good the car is.

All the many books available on how to calculate the MOS can be obtained and studied closely and it would still be very difficult (and I’m not kidding here) to find a solution for the MOS. That is why what Nick provided us with is a gift.

Because we don’t know how to work out the MOS, many times we are buying shares at £2 or £3 on the pound. That is like going back to that BMW garage and buying that same car, but now for £80,000 or even £120,000. That sounds like a silly thing to do, but we do it when we buy shares!

I was wrong to provide a suggested timeframe for longer term shares. It seems that some have latched onto that guidance I gave – when really it’s an individual interpretation of what is longer. My suggestion allowed for a purchase at any point in the market cycle. But I don’t know, and nor does the buyer probably, at what point in a market cycle they are at time of purchase.

As for Buffett being an investing dinosaur, the methodology comes from Graham, and he was the generation before Buffett. But in any case, it’s nothing to do with either of them really. Buying something for fifty cents on the dollar is as good a market trading philosophy today as it was in Babylonian times.

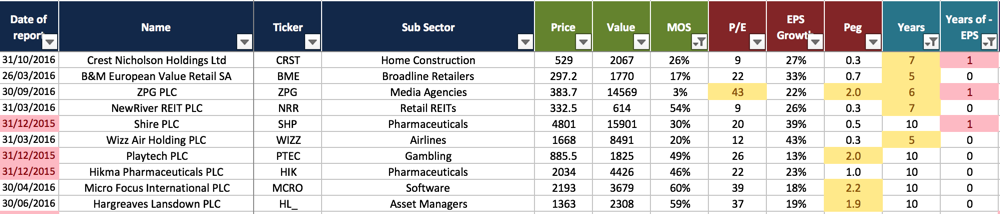

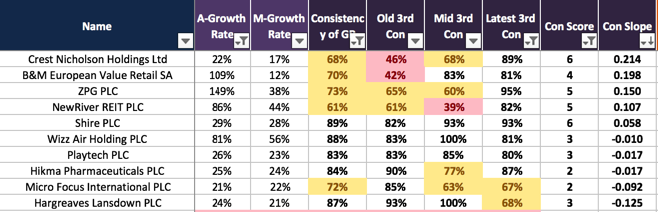

As for Blackberry, this was given as an example only of what to watch out for. Kodak is another. It doesn’t matter here about these companies. I was merely trying to say that such companies can show up on Nick’s list but are about to crash. That is why Nick has provided the 1st, 2nd and 3rd periods of measured consistency to help us spot such companies. And for those who think it’s easy to see such companies coming, sure it is after the fact, but most of the brightest analysts in the world didn’t at the time.

Market cycle is worth a further mention here. I’m not a doom and gloom thinking guy, quite the opposite actually. Benjamin Graham gave up at one point because he couldn’t find companies that provided value, a MOS. This was prior to the great depression. From 350 companies we would expect to find about 10% with a qualifying MOS. On the last run 3% qualified, and some of those are questionable as they don’t have the 10 years of reports.

I don’t recall any of my chart analysis providing a ‘buy me now signal’ either. Moreover, once the daily press has front page news telling us it’s a great time to buy – well, you know what I think about that.

With 5-minute bar charts I deal with a major trend reversal a few times a week. With such a chart it would not be possible without the X/Y values showing to tell the difference between this and, say, the 2008 market crash on a weekly chart. So the short-term trader gets a lot of experience with market reversals.

More often than not, a beginner trader will trade a reversal too early (this is the case for both short and long-term trading/investing). Only to be stopped out at a higher price – in the case of a bull reversal – and watch from the sidelines as the market eventually drops. On a 5-minute chart such a reversal can take hours, on a weekly or monthly chart it is years – or at the very least many months.

As a final thought, value investing, or the interpretation of fundamentals, is not generally considered a suitable methodology for mid-term investing. There are alternatives. For example: taking advantage of IPOs, share splits or runaway news, events, fads and fashions. I particularly like the interpretation of the COT report with commodities for mid-term investment.

I hope this helps.