Let us chat strategy for a moment. Wikipedia says strategy “is a high level plan to achieve one or more goals under conditions of uncertainty.”

Many that provide trading strategies have it wrong. What they are actually providing is a way to trade, or a method, or a system. The way that I trade is contained within my ‘algorithm to trade by’ page and this is something I tinker with all the time. (I call it an algorithm so that I keep in mind that I’m up against algo-trading which is unemotional, timely and precise).

What I don’t tinker with, however, is my strategy; well, at least not without a great deal of consideration. A strategy is to be clear:

- Multiple swing

- Swing

- Swing/scalp

- scalp

(traders interpret a swing and a scalp differently, see ‘algorithms to trade by’ in the paragraph clarification)

I may use a multiple swing strategy for very long-term value investing such as with Nick’s top FTSE 350 shares; a swing only strategy is perfect for intermediate traders or experts not intraday or unable to watch the trade; swing/scalp (my passion) is the full-time experts choice; and scalp only is, well, a difficult strategy because of the often poor reward/risk ratio.

As I’m a swing/scalp strategist I also sub-divide that strategy into swing/scalp or scalp/swing; taking the first more determinedly than the second, but that’s for another time.

Each strategy requires little understanding, just rationality in comparing two outcomes (price up, price down), exercising the better option and holding for the desired target. I get out at break even if my algorithm tells me to. It’s about control of the downside and then about the maximisation of the upside.

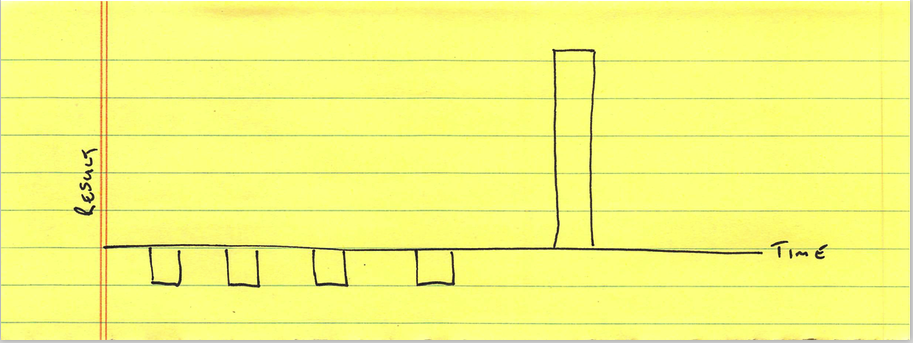

The first sketch below was used by Steve Jobs at one of his presentations to show how he took (many) minimal downsides before he eventually got the big upside.

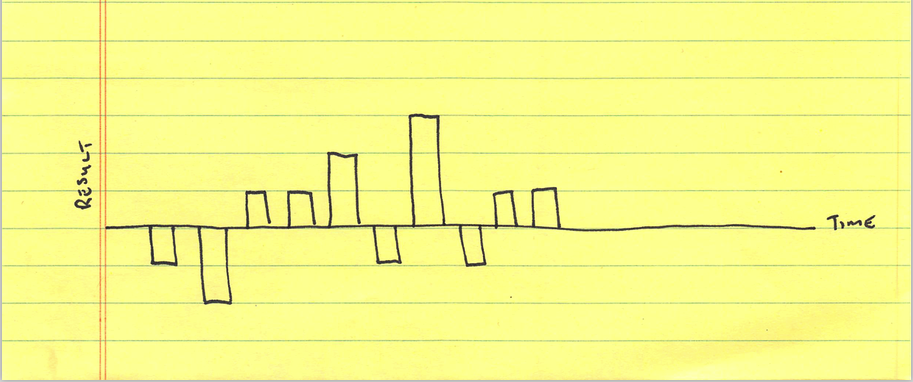

The same is for good trading. The next sketch might represent how much was made or lost each year with a longer term investment. If we checked the results, say, every three years we would only once see a decrease in our year on year portfolio results, therefore minimising emotional drain. Each blue horizontal line might represent a £1,000 (or multiples of) year on year profit or loss.

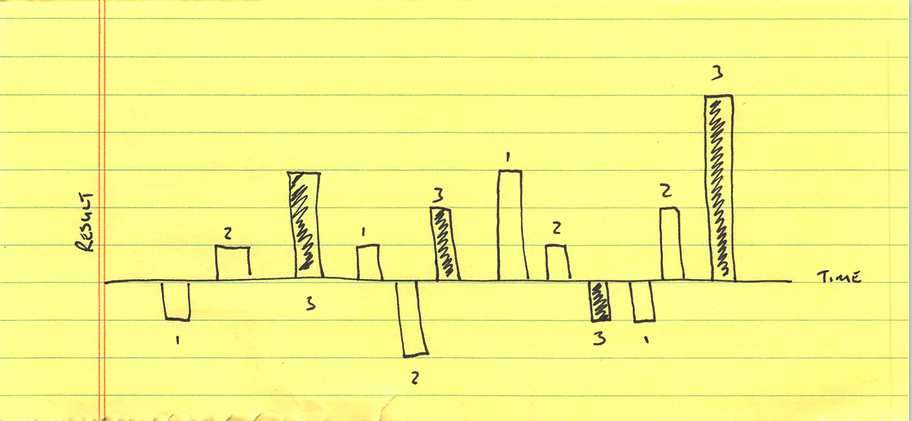

Finally, a sketch of a day traders result for the day. A single blue horizontal line up or down represents a scalp win or loss; two horizontal lines is a swing. The bar with three horizontal bars up was a swing that was entered early and provided the extra profit. We should never see more than two bars at any one time to the downside. Each swing and scalp, therefore each horizontal blue bar, is the same in value whether the scalp was 10 pips or 30 pips. Each horizontal line represents the traders risk. A traders risk (each horizontal line) might be £60, or £600, or £6,000 – or any figure in between – depending on the traders account. But it has to be consistent.

The point here is that any downside (for the sake of emotional drain and our pocket) has to be known, acceptable and controlled. This is something most of us don’t understand when we start out. Steve Jobs understood this and he did okay.